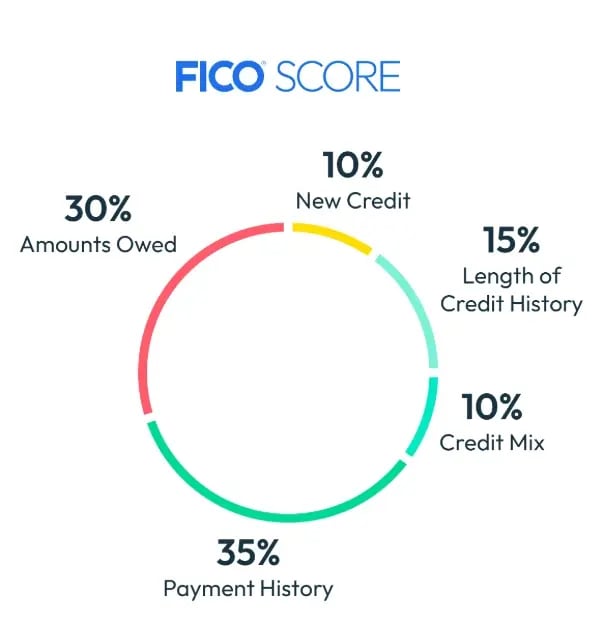

Your credit scores are built from multiple factors, but one carries more weight than any other: your payment history. Under VantageScore 3.0, the model ScoreSense displays, payment history accounts for roughly 40% of your score. Under FICO, it sits at 35%. Either way, no other input matters more.

That weight exists because the credit bureaus treat your past behavior with credit as the strongest available signal of how you'll handle credit going forward.

Quick Breakdown

- Payment history is roughly 40% of your VantageScore 3.0 credit score and 35% of your FICO score.

- Most creditors report payment activity to the three credit bureaus once a month.

- A payment generally has to be 30 or more days past due before it can be reported as late.

- Late payments can stay on your credit reports for up to seven years from the original delinquency date.

- Consistent on-time payments across all accounts are a key factor in how payment history is reflected in your credit reports.

What Is Payment History?

Your payment history is the record of how consistently you've paid your credit obligations on time. It tracks every account that reports to the credit bureaus, month by month, across years. Paying bills by the due date is reflected as positive payment activity on your credit reports

Paying bills by the due date is reflected as positive payment activity on your credit reports. Miss a payment, or pay it well after the due date, and that record takes a hit.

A single late payment may only nudge your credit scores. Repeated or habitual late payments compound, and the effect grows the longer an account stays delinquent. Credit profiles with higher scores commonly show the same underlying habit: consistent on-time payments, every cycle, across every open account.

How Much Does Payment History Affect Your Credit Score?

The two scoring models most lenders use weigh payment history slightly differently, but both rank it as the single largest factor.

VantageScore 3.0 weighs its six factors approximately as follows:

- Payment History: about 40%

- Account Mix and Credit Age: about 21%

- Credit Utilization: about 20%

- Balances and Debt: about 11%

- New Activity: about 5%

- Available Credit: about 3%

FICO weighs payment history at 35% of its score, followed by amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit (10%).

The takeaway is the same in either model. Payment history is the heaviest variable. Because it carries significant weight, changes in payment history may influence your credit scores.

Get My 3-Bureau Credit Reports and Scores

Payment History as a Measure of Creditworthiness

Lenders, landlords, and insurers look at payment history because it answers the question they actually care about: does this person pay what they owe, on time?

Credit scoring models translate that question into math. They count how many of your accounts have ever been late, how late those payments were, how recently those late payments occurred, and how many accounts are currently in good standing. The output, expressed as your credit score, is the model's best estimate of how likely you are to repay future credit on time.

That is why payment history is treated as a measure of creditworthiness. Every other factor (utilization, account age, credit mix) speaks to your borrowing capacity or experience. Only payment history speaks directly to your follow-through.

What Accounts Show Up in Your Payment History?

Your credit reports include payment activity for most credit-based accounts, including:

- Credit cards

- Mortgage loans and home equity lines of credit (HELOCs)

- Auto loans

- Student loans

- Personal loans

- Retail credit accounts

- Finance company accounts

- Collections accounts (when an unpaid debt is sold or referred to collections)

Some payment activity does not consistently appear on your credit reports. Rent, utilities, and cell phone bills typically only show up if the landlord, utility, or carrier reports them, or if a missed payment is sent to collections.

How Is Payment History Calculated?

The credit bureaus build your payment history from data your creditors report, usually once per billing cycle. A payment that is a few days late often does not get reported as late at all. The reporting thresholds matter:

- 30 days past due: the creditor can report the payment as late to the bureaus. This is when most consumers see the first credit score impact.

- 60 days past due: a more severe late notation is added, and score impact deepens.

- 90 days past due: another tier of severity, and at this point the account is often headed toward charge-off.

- 180 days past due: federal regulations require most creditors to charge off the account. The charge-off itself is reported and stays on your credit reports for up to seven years from the date of original delinquency.

Once a late payment is reported, several factors influence how much it affects your credit:

- How late the payment was (30, 60, 90, or 120-plus days)

- How recent the late payment is (newer is more impactful)

- How many late payments are on your reports overall

- How much you currently owe on delinquent or collections accounts

- Whether other adverse events appear on your reports, such as charge-offs or bankruptcies

- How many of your other accounts are currently in good standing

The Consumer Financial Protection Bureau publishes consumer-facing guidance on how late payments are reported and how long they remain on your credit reports.

How Long Do Late Payments Stay on Your Credit Reports?

Under the Fair Credit Reporting Act, most negative payment information can remain on your credit reports for up to seven years from the date of the original delinquency. That includes 30, 60, 90, and 120-plus day lates, as well as charge-offs and most collections.

A few important nuances:

- The seven-year clock starts at the original delinquency date, not the date the account was charged off, sold to a collection agency, or last updated.

- A debt that has aged off your credit reports is not erased as a debt. The legal obligation to repay generally still exists, depending on your state's statute of limitations and the type of account. Aging off the report and being legally satisfied are two different things.

- Bankruptcies follow a different timeline. Chapter 7 bankruptcies can remain on your credit reports for up to 10 years. Chapter 13 typically falls off after 7 years.

If you find a late payment on your credit reports that should not be there, you have the right to dispute it directly with the bureau. The ScoreSense Dispute Center provides step-by-step guidance to help members file disputes themselves with Equifax, Experian, or TransUnion.

Practices That Support Positive Payment History

You cannot rewrite past late payments, Future payment activity will continue to be reflected in your credit reports over time. A few habits do most of the work.

- Pay every bill on time, every cycle. This sounds obvious. The execution is the hard part. Build a budget that protects minimum payments first, then everything else. Be aware that some bills are reported to the credit bureaus and others may not be.

- Set up autopay for at least the minimum. Even if you pay more manually each month, autopay on the minimum is a safety net against a missed due date during a busy week or a travel stretch.

- Contact your creditors before you fall behind, not after. Lenders and card issuers often have hardship programs, payment deferrals, or interest-rate concessions for customers who reach out proactively. The conversation is much harder once the account is already 60 days past due.

- Avoid taking on new credit while you're catching up. Adding a new monthly minimum to a budget that's already strained tends to make on-time payment harder, not easier.

- Use credit monitoring to catch mistakes early. Errors and unauthorized accounts on your credit reports can drag down your payment history. The faster you spot them, the easier they are to address.

These steps support credit health strategies broadly. They are not a guarantee that any specific score change will follow, since credit scoring models weigh many variables.

Tracking Payment History with ScoreSense

ScoreSense provides daily credit monitoring through Experian, with monthly score updates from all three bureaus that members pull when they sign in. Identity theft monitoring and up to $1 million identity theft insurance policy underwritten by AIG are available as upgrades to the membership.

FAQ

Is payment history really 40% of your credit score?

Under VantageScore 3.0, the model ScoreSense displays, payment history accounts for approximately 40% of the score. Under FICO, it accounts for 35%. The exact percentage depends on which model is being used, but in every major consumer credit scoring model, payment history is the largest single factor.

How long does one late payment stay on your credit report?

A reported late payment can remain on your credit reports for up to seven years from the date of the original delinquency, per the Fair Credit Reporting Act. The score impact tends to fade over time, particularly as the late payment ages and as you build a record of on-time payments after it.

Does paying off a collection remove it from your credit report?

Not automatically. Paying off a collection account typically updates the status to "paid" but does not remove the account from your reports. The collection can stay on your reports for up to seven years from the original delinquency date that triggered the collection. Some newer scoring models weigh paid collections less heavily than unpaid ones. If you believe a collection is reporting in error, the ScoreSense Dispute Center walks you through filing a dispute with the bureau.

Will paying off a debt change my credit score?

It can produce a score change, but the direction and size depend on the specifics. Paying off a credit card balance typically reduces utilization, which may positively affect your score. Paying off a collection or charge-off updates the status of the account but does not erase it. The exact score change varies by individual and by scoring model. ScoreSense's ScoreCast provides estimates of how certain actions may be reflected in score changes.

What's considered a good payment history?

A consistent record of on-time payments across all your active accounts, with no late payments in recent months and ideally no late payments in the past two years, is generally considered strong. Members with credit scores of 810 or above, the threshold for excellent credit on most VantageScore models, almost universally show clean recent payment history.

How do I report on-time rent or utility payments to the credit bureaus?

Rent and utilities are not automatically included in your payment history. Some landlords and utility companies report through third-party services, and several consumer-facing services let renters opt into reporting their on-time rent payments. Check with your landlord or utility provider to see whether they participate, and verify which bureaus the reporting service shares data with. You can also see whether those payments are showing up on your reports by reviewing all three bureau reports inside ScoreSense.