Your credit score is a three-digit number that summarizes your credit risk at a given point in time (when you check it).

Every score falls somewhere on a defined scale, and where it lands determines how lenders may treat you: whether you get approved, what interest rate you pay, and in some cases whether you qualify at all.

This article breaks down how VantageScore 3.0 and FICO structure that scale, what each range means in practice, and what factors actually move the number.

The Quick Breakdown

- Credit scores range from 300 to 850 under both VantageScore 3.0 and most FICO base models. Lower scores represent higher risk. Higher scores represent lower risk.

- ScoreSense uses VantageScore 3.0, which organizes that range across six tiers from Very Poor to Excellent.

- VantageScore and FICO use the same range but different breakdowns for what counts as good, fair, or poor, and they weight the factors differently.

- A few points can matter significantly when lenders use score thresholds to determine approval or rate tiers.

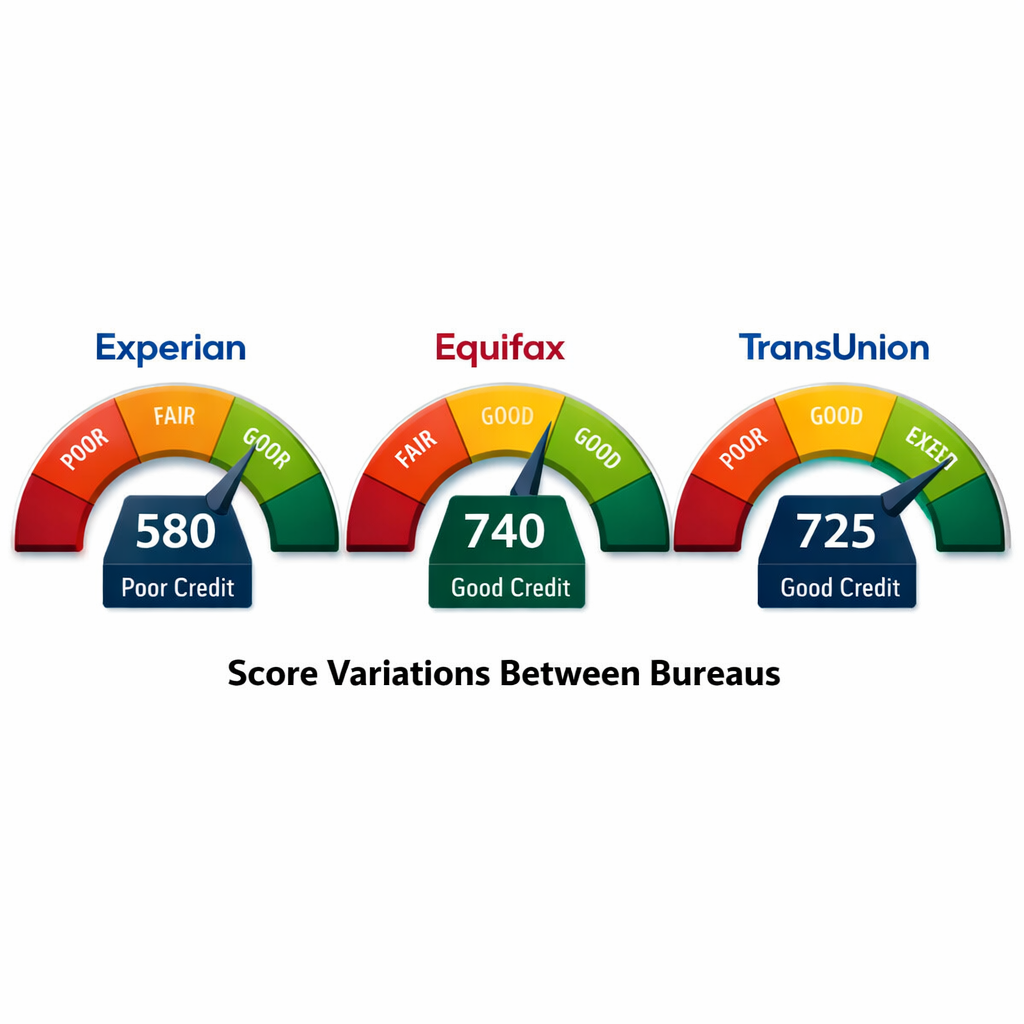

- Scores can differ across the three bureaus because not all creditors report to all three. Checking all three gives you the complete picture.

Credit Score Ranges

Credit scores typically range from 300 to 850. A score of 700 or higher is generally considered good, though the specific threshold varies by lender and by which scoring model they use. Understanding where your score falls and what it signals is the first step toward understanding it.

Two of the most widely used credit scoring models are VantageScore and FICO. Both organize scores on a numerical scale with labeled tiers such as poor, fair, good, and excellent, but the breakdowns are not identical.

What one lender considers good, another might rate as fair, depending on which model they use. In the end, it's all situational and sometimes lender preference.

Get My 3-Bureau Credit Reports and Scores

VantageScore Ranges

VantageScore was created in 2006 by the three major credit bureaus: TransUnion, Experian, and Equifax. The goal was a more consistent, consumer-friendly model that could score more people than FICO.

VantageScore 4.0 is now the most widely used version of the model, though VantageScore 3.0 remains in broad use. ScoreSense uses VantageScore 3.0 to calculate the scores shown in your dashboard. It scores on a range of 300 to 850. Here is how the range breaks down:

- Excellent Credit: 810-850

- Great Credit: 750-809

- Good Credit: 670-749

- Fair Credit: 560-669

- Poor Credit: 500-559

- Very Poor Credit: 300-499

VantageScore 3.0 weighs six factors when calculating your score. In order of impact:

- Payment History

- Account Mix and Credit Age

- Credit Utilization

- Balances and Debt

- New Activity

- Available Credit

This differs from FICO's five-factor structure, which matters if you are trying to understand why the same credit behaviors can move your VantageScore and your FICO score differently.

FICO Score Ranges

The FICO model has been used in lending decisions since 1989. FICO generates both base scores and industry-specific scores used for mortgage, auto, and credit card applications.

Most FICO base scores use a range of 300 to 850, though some industry-specific FICO models extend beyond 850. The most widely used base version is FICO 8. Here is how the standard base score range breaks down:

- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

VantageScore Model vs. FICO Model

Although VantageScore and FICO share some foundational similarities, there are meaningful differences between them worth understanding.

Basic Similarities

Score Ranges: Both VantageScore and FICO score on a range of 300 to 850 with similar tier labels.

Credit File Sourcing: Both gather consumer credit files from TransUnion, Equifax, and Experian.

Rating Criteria: Payment history carries the most weight in both models. VantageScore 3.0 uses six factors, while FICO uses five, and the specific labels and weightings differ between them.

Paid Collection Accounts: Under VantageScore, paid collections are weighted less heavily than unpaid ones, which means resolving a collection can produce a meaningful score impact. Under FICO 9, paid collections are ignored entirely, but many lenders still use FICO 8, where paid and unpaid collections carry similar weight (source).

Multiple Credit Inquiries: Both FICO and VantageScore recognize rate-shopping behavior. Multiple hard inquiries for the same loan type within a short window are typically counted as a single inquiry.

Primary Differences

Scoring Requirements: VantageScore's model can score approximately 30 to 35 million people who would be considered unscorable by FICO.

- FICO requires at least six months of credit history and at least one account reported within the last six months.

- VantageScore requires only one month of credit history and one account reported within the past two years.

- VantageScore accepts alternative data such as rent, utility, and phone payments reported to the bureaus. FICO does not.

Factor Structure: VantageScore 3.0 uses six weighted factors. FICO uses five. The labels and weightings differ between the two models, so the same change to your credit file can affect each score differently.

Other Credit Scores

Although VantageScore and FICO are the most widely used credit scoring models, others exist. All models share one common theme: a lower score indicates greater risk, and a higher score indicates lower risk.

Two other scoring models worth knowing:

TransUnion New Account Score 2.0: Range of 300-850. Financial institutions use this model to manage existing accounts. It predicts the likelihood that specific consumers will default within the next three months.

Experian's PLUS Score: Range of 330-830. The PLUS score is developed by Experian for consumer educational use only. It is sometimes offered for free online but is not used by lenders for credit decisions.

What Is a Good Credit Score?

Under VantageScore 3.0, a good credit score is 670 or higher. Under FICO 8, a good score also starts at 670. Scores of 750 and above reflect strong credit standing.

What Is a Bad Credit Score?

Under VantageScore 3.0, any score below 560 falls in the poor or very poor range. Under FICO 8, a score below 580 is considered poor. In either model, scores in this range signal elevated risk to lenders and can limit approval options or result in significantly higher interest rates.

When a Few Points Can Make a Big Difference

Depending on the type of loan, borrowers may need to meet specific score thresholds to qualify. If the minimum to qualify for a given loan is 580 and your score is 579, you will be denied, regardless of how close you are. A few points can be the difference between approval and rejection, or between a lower rate and a higher one.

Lenders use risk-based pricing, meaning the rate you receive reflects the risk you present. A borrower with a score in the excellent range will typically qualify for significantly better rates than one in the fair range, and the difference compounds over the life of a loan.

How Does Your Credit Score Affect Your Life?

Your credit score affects your ability to borrow money and the cost of that borrowing. Here is what each range generally means in practice:

People with very good and excellent credit scores may be:

- eligible for better interest rates, payment terms, and options than consumers with lower scores

People with fair to good credit scores may be:

- more likely to be approved than those with poor credit

- able to choose from a wider selection of lending options and offers

- less likely than those with higher scores to qualify for the best available rates

People with poor credit may be:

- less likely to be approved for loans or credit cards

- more likely to be offered higher rates and fewer options than those with higher scores

What Impacts Your Credit Score, and What Does Not

Factors that impact your credit score (VantageScore 3.0):

- Payment history

- Account mix and credit age

- Credit utilization

- Balances and debt

- New activity

- Available credit

Factors that do not impact your credit score:

- Checking your own credit

- Income

- Net worth

- Age

- Education

- Criminal history

- Marital status

- Location

- Debit card use

- Whether you receive government benefits

Lenders Look at More Than Credit Scores

Although your credit score matters, a lender's decision is not based on that number alone. Lenders commonly review:

Income: Lenders want to see that you can repay your debts. Little or no income increases perceived risk and can lead to denial.

Employment: Long tenure at a single employer signals stability. Frequent job changes can raise concerns about reliability.

Down payment: A larger down payment reduces the lender's exposure. If your score is not strong, a significant down payment may help secure approval or a better rate.

Capital available: Liquid assets demonstrate that you could cover payments in the event of a financial disruption, which lowers perceived risk.

Length of time in your residence: Stability in your living situation can signal financial responsibility to lenders.

Student loan debt: A significant debt load relative to income may affect how lenders assess your capacity to take on additional credit.

What Does Your Credit Score Range Mean for Borrowing?

Understanding where your score falls is a starting point. But lenders apply credit score ranges differently depending on the loan type, the institution, and the scoring model they pull. Here is what the tiers generally signal:

- Great (750 and above under VantageScore 3.0): You are likely to qualify for the most competitive rates. Lenders view you as a low-risk borrower.

- Good (670 to 749): Most mainstream lenders will approve you. Rate offers will be solid, though not always at the lowest tier available.

- Fair (560 to 669): Approval is possible but you may face higher rates, stricter terms, or a larger down payment requirement.

- Poor (below 560): Approval becomes selective. Some lenders specialize in this range, but rates will be significantly higher and terms more restrictive.

One important note: the score you see in ScoreSense reflects VantageScore 3.0. Many lenders, particularly mortgage lenders, use FICO models instead. The same underlying credit behavior can produce different scores depending on the model, which is why your scores and reports together tell a more complete story than any single number.

Get My 3-Bureau Credit Reports and Scores

Frequently Asked Questions

What is the credit score range?

Credit scores typically range from 300 to 850 under both VantageScore 3.0 and most FICO base models. A score of 300 represents the highest credit risk, and 850 the lowest. Some industry-specific FICO models use a wider range, but 300 to 850 covers the vast majority of scores consumers encounter.

What is a good credit score?

Under VantageScore 3.0, a good score is 670 or higher. Excellent starts at 810. Under FICO 8, the good range also begins at 670, while excellent starts at 800. The definition of good ultimately depends on the lender and the scoring model they use.

What credit score does ScoreSense show?

ScoreSense shows your VantageScore 3.0 from all three bureaus: TransUnion, Equifax, and Experian. VantageScore 3.0 uses a range of 300 to 850 and is one of the most widely used consumer scoring models available. The score shown in ScoreSense may differ from the score a specific lender pulls, since lenders use different models depending on the loan type.

What is the difference between VantageScore 3.0 and FICO?

Both models use a range of 300 to 850 and draw data from the same credit bureaus. The main differences are in scoring requirements, factor structure, and range tier definitions. VantageScore 3.0 can score people with as little as one month of credit history; FICO requires at least six months. VantageScore 3.0 uses six weighted factors; FICO uses five. The two models also define the cutoffs for good, fair, and poor credit at slightly different points.

Why does my credit score vary across the three bureaus?

Each bureau collects its own data. Not all creditors report to all three, and information can update at different times. As a result, your VantageScore 3.0 can differ meaningfully across TransUnion, Equifax, and Experian. A collection account or missed payment may appear on two reports and not the third. Seeing all three at once is the only way to know what each bureau is actually reporting.

Does checking my credit score affect it?

No. Checking your own credit is a soft inquiry and does not affect your score under any mainstream scoring model. Only hard inquiries, initiated when you apply for new credit, can have an impact.

What credit score do I need for a mortgage?

Requirements vary by lender and loan type. FHA loans can allow scores as low as 500 with a larger down payment, or 580 with a standard down payment. Conventional loan programs generally require higher minimums. The rate a lender offers also depends on your score tier, with lower scores typically producing higher interest rates over the life of the loan. Ask your lender which scoring model they use before drawing conclusions from your VantageScore alone.

What does VantageScore 3.0 use to calculate my score?

VantageScore 3.0 uses six factors: Payment History, Account Mix and Credit Age, Credit Utilization, Balances and Debt, New Activity, and Available Credit. Payment history carries the most weight, which means consistent on-time payments are the single most important habit for maintaining a strong score.

Why Monitoring Your Scores and Reports Matters

Your credit score is a snapshot, not the full picture. Because creditors report to bureaus independently, a missed payment, charge-off, or new collection account may appear on one report and not another. Checking all three gives you visibility into everything that lenders may review.

ScoreSense gives you access to your credit scores and reports from all three bureaus: TransUnion, Equifax, and Experian. Because ScoreSense uses VantageScore 3.0, the scores shown reflect one of the most widely used consumer scoring models available. If something changes on your Experian report, you will receive an alert. ScoreTracker shows how your scores move across all three bureaus over time, so progress and recovery are visible as they happen rather than only in hindsight.