Quick Breakdown

- A voluntary repossession is still a loan default and stays on your credit report for seven years

- The credit score impact comes mostly from missed payments and the repossession entry itself, not from the choice to surrender voluntarily

- A voluntary surrender can be noted on your tradeline and may provide context to future lenders reviewing your report, but it does not meaningfully change your score

- Any deficiency balance after the lender sells the vehicle can become a separate collection account, which extends the credit damage

- The debt remains legally owed throughout the seven-year reporting window, regardless of how the vehicle is recovered

When you can no longer afford a car payment, handing the keys back to your lender can feel like the responsible move. It is also still the default move.

A voluntary repossession sits on your credit report for seven years, the same window as an involuntary one, and it carries most of the same score consequences. Many people don’t realize that detail.

The difference between the two is smaller than people expect, and understanding what actually happens to your credit reports and scores helps you decide whether voluntary surrender is the right call.

How a Voluntary Repossession Affects Your Credit Report

A repossession does not show up as a single line item. It usually triggers a chain of negative entries that build on each other.

Missed payments leading up to the surrender

Most voluntary repossessions follow a stretch of missed or late payments. Each payment that lands more than 30 days past due gets reported, and Payment History accounts for roughly 40% of your VantageScore 3.0 score. The damage starts well before the surrender itself.

The repossession entry

Once the vehicle is surrendered, the original auto loan account is typically closed and noted as a repossession. Even when you initiated the handoff, the tradeline reflects that the loan was not paid as agreed. This is the entry that stays on your credit report for seven years from the date of the original delinquency.

Collection accounts and the deficiency balance

When the lender sells the vehicle at auction, the sale price often covers less than what you still owed on the loan. The gap, called a deficiency balance, is still your responsibility.

If you cannot pay it, the lender often sells or transfers the balance to a collections agency, which adds a separate collection tradeline to your credit report.

Collection accounts can remain for seven years from the original delinquency, even if you eventually pay the balance off. If a tradeline contains errors, the ScoreSense Dispute Center walks you through filing disputes with each bureau directly.

Lawsuits over the deficiency

If the deficiency balance goes unpaid long enough, the lender or collection agency can sue you for it. A lawsuit can result in a court judgment ordering repayment.

Civil judgments stopped appearing on most consumer credit reports after the National Consumer Assistance Plan changes took effect in 2017, but the underlying debt and any related collection accounts still appear. A judgment also creates consequences outside your credit file, such as wage garnishment in states that allow it.

How Much Can a Voluntary Repossession Lower Your Credit Score?

There is no single number.

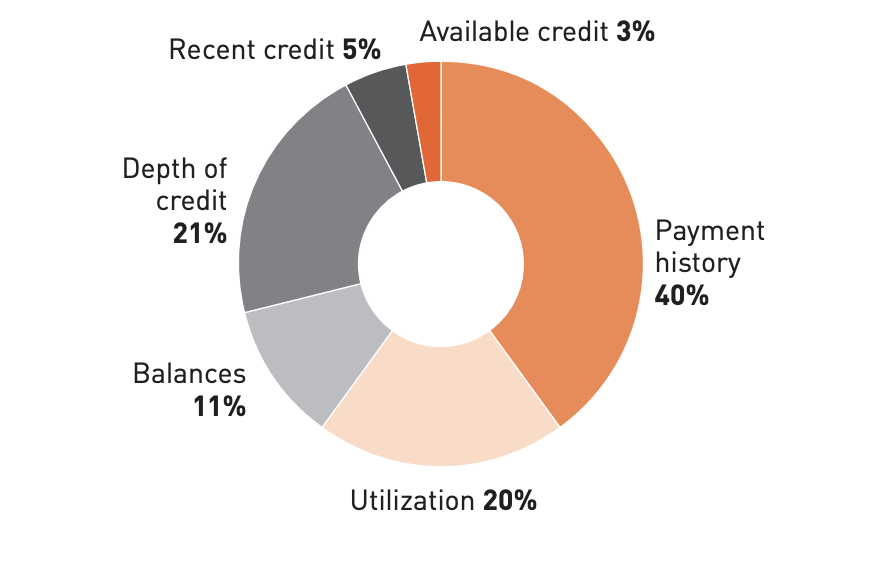

The score change depends on where you started, how many payments you missed before the surrender, and what the rest of your credit profile looks like. VantageScore 3.0 weights its score factors roughly as follows:

Payment History (40%),

Account Mix and Credit Age (21%),

Credit Utilization (20%),

Balances and Debt (11%),

New Activity (5%),

Available Credit (3%).

A repossession touches several of these at once. It is a serious payment history event, it ages and closes a tradeline, and the resulting collection account introduces another derogatory entry on top.

People who already have strong credit usually see a larger numerical drop than people whose scores are already low, simply because there is more distance to fall. Either way, the score change is meaningful, and your borrowing options will narrow for some time afterward. Tracking month-over-month movement with a tool like ScoreTracker helps you see when the lowest point passes and how consistent on-time payments on remaining accounts are reflected in your credit history over time.

Voluntary vs Involuntary Repossession: What's Different on Your Credit

The biggest myth about voluntary repossession is that it spares your credit. It does not. Both versions appear as repossessions on your credit report, both stay for seven years, and the credit score impact is essentially the same.

What can differ:

- Notation on the tradeline. Some lenders mark the account as voluntarily surrendered. A future lender reviewing your report can see you took action rather than letting the lender chase the vehicle. This is a soft signal, not a score factor.

- Out-of-pocket cost. Involuntary repossessions usually add towing, storage, and recovery fees to the deficiency balance. Voluntary surrender often avoids those.

- Timing and stress. With voluntary surrender you set the handoff. With involuntary repossession, a recovery agent can take the vehicle from your driveway, your workplace, or a parking lot, often without warning. The Federal Trade Commission notes that in most states a lender can pursue repossession the moment you default, with limited notification requirements.

What does not differ:

- The seven-year reporting window

- The fact that the deficiency balance is still legally owed after the sale

- The size of the score impact in any practical sense

If you are weighing voluntary against involuntary, weigh it on cost, stress, and timing. Do not weigh it on the assumption that one will leave your credit meaningfully better off than the other.

Other Scenarios People Ask About

Voluntary repossession and business credit

If the loan is in your business's name and the business is the borrower, the repossession is normally reported on business credit files (Dun & Bradstreet, Experian Business, Equifax Business) rather than your personal credit. If you personally guaranteed the loan, which is common for small businesses, the lender can pursue you personally for the deficiency, and a resulting collection account or judgment can land on your personal credit too. Mixed structures are common, so reviewing the loan documents is the only reliable way to know which credit file is exposed.

Voluntary repossession on a personal loan or non-auto loan

The word repossession typically refers to secured loans. If a personal loan is unsecured, there is no collateral for the lender to take back. The default still hits your credit, and the unpaid balance can be sold to collections, but there is no surrender to arrange. If a personal loan is secured by collateral such as a boat, equipment, or a second vehicle, the same voluntary surrender option exists, and the credit consequences mirror those of an auto loan.

Voluntary surrender as a strategic move

Some borrowers consider voluntarily surrendering a vehicle they could still afford, expecting the lender to write off the balance. Lenders rarely do, and the credit damage is real. The debt remains legally owed regardless of how the vehicle is recovered, and the seven-year credit reporting window applies the same way.

Ways to Avoid a Repossession

Letting payments slip without contacting your lender is the worst of the available options. Once you go past about 60 to 90 days without payment, repossession becomes a real possibility in most states. Acting earlier widens your choices.

Call your lender

A call before you miss a payment carries more weight than a call after you have missed three. Lenders sometimes offer a deferment, a temporary interest-only period, or a loan modification that extends the term and lowers the monthly payment. None of those options are guaranteed, and not every lender offers them, but you cannot use what you do not ask for.

Refinance the loan

If your credit is still in reasonable shape and the vehicle is worth close to what you owe, refinancing the auto loan with another lender can lower the rate and the payment. The further behind you fall, the harder this gets, so refinancing is most useful as an early-warning move, not a last-resort one.

Apply for a hardship program

Some lenders, especially credit unions and larger banks, run formal hardship programs for borrowers facing job loss, medical events, or natural disasters. The Consumer Financial Protection Bureau has guidance on auto loan hardship options if you need a starting point for the conversation with your lender.

Sell the vehicle yourself

Selling the car privately and using the proceeds to pay off the loan avoids a repossession entirely. This works cleanly when the sale price covers the loan balance. If the sale falls short, you are responsible for the difference before the lien is released, so this strategy works best when you have positive equity or a balance close to zero.

Ways to Get Your Car Back After a Repossession

If your situation changes after the surrender, you may be able to recover the vehicle, but the window is short and the rules vary by state.

- Reinstatement. Some states require lenders to allow you to reinstate the loan by paying the past-due amount plus repossession fees. The loan continues on its original terms.

- Redemption. You can pay off the entire remaining loan balance plus repossession costs and reclaim the vehicle. This is expensive and requires cash that most borrowers in this situation do not have on hand.

- Buying at auction. In many states the lender must notify you of the planned sale, including the auction date and location. You can attend and bid like any other buyer, although you will need cash or financing in place to do so.

Each option depends on your state's laws and the specific terms of your contract. Read the post-repossession notice from your lender carefully, since it lists your rights.

Monitoring Your Credit After a Repossession

A repossession affects multiple lines on your credit report, sometimes in stages, and watching those changes lets you catch reporting errors early. ScoreSense gives members access to credit reports and scores from all three credit bureaus, with daily credit monitoring on your Experian file. Score updates are prepared monthly, and logging in pulls the latest one.

If a tradeline shows the wrong amount, the wrong dates, or a status that does not match what your lender told you, the ScoreSense Dispute Center walks you through filing disputes with each bureau directly. ScoreSense does not file disputes on your behalf, but the step-by-step guidance covers what each bureau requires from you.

You can also pull free annual reports at AnnualCreditReport.com to confirm what each bureau is reporting. ScoreCast and Credit Insights help you see how specific actions, like clearing the deficiency balance or keeping other accounts current, may affect your score over time.

FAQs

How much does voluntary repossession hurt your credit score?

The score change varies based on where your score started and how many payments you missed before the surrender. Higher scores generally see a larger numerical drop, since they have further to fall.

A repossession affects multiple VantageScore 3.0 factors at once, including Payment History (around 40% of the score), and any resulting collection account adds another negative entry on top of the repossession itself.

Does voluntary repossession hurt credit less than involuntary?

Not in any meaningful way for your score. Both appear as repossessions on your credit report, and both stay for seven years. A voluntary surrender may be noted on the tradeline, which a future lender can see, but the score impact is essentially the same.

How long does a voluntary repossession stay on your credit report?

Seven years from the date of the original delinquency that led to the repossession. Any related collection account or deficiency balance has its own seven-year clock, also tied to the original delinquency.

Does voluntary repossession affect business credit?

If the loan was taken out by the business and is in the business's name, the repossession is normally reported on business credit files rather than your personal credit. If you personally guaranteed the loan, the lender can pursue you for the deficiency, which can show up on your personal credit through a collection account or judgment.

Can you get your car back after voluntary repossession?

Sometimes, depending on your state and your contract. Reinstatement (paying the past-due amount plus fees) and redemption (paying off the full loan balance plus fees) are the two most common paths. In many states the lender must also notify you of the auction date, where you can bid on the vehicle.